Expat Banking Guide: Essential Steps for Global Living 2026

Discover the art of expat banking in 2026 with expert steps for seamless global living Prepare your finances choose the right accounts manage currency and thrive

The world is more connected than ever, and with this global freedom comes the thrill and complexity of managing your money across borders. For many, expat banking in 2026 is both an opportunity and a challenge, as shifting regulations and digital tools reshape how we live and thrive abroad.

Imagine landing in a new country only to find your home account frozen or your transfer delayed. These are real hurdles, but with the right expat banking strategy, you can turn obstacles into empowerment. Streamlined finances mean less stress, more confidence, and the ability to seize every adventure.

This guide reveals the essential steps to master expat banking: preparing your finances, choosing the right accounts, managing currency, securing access, and staying ahead of evolving rules. Follow along for clarity, peace of mind, and true global flexibility.

Step 1: Prepare Your Finances Before Moving Abroad

Navigating expat banking starts long before your plane takes off. The journey to financial confidence begins with a clear-eyed look at your current resources and the unique demands of life abroad. Picture this as charting a map before a grand voyage, ensuring every crossing is smooth and every port welcoming.

Assess Your Financial Situation

Begin your expat banking journey by taking inventory of all financial accounts, credit cards, and outstanding loans in both your home and future host country. List every income source, from salaries to investment returns, and forecast your typical expenses for both locations.

Visualize your cross-border cash flows using a simple spreadsheet or a financial app. This clarity allows you to spot gaps and plan for seamless transitions. For example, someone moving from the UK to Germany might list their GBP savings, pension income, and anticipated EUR expenses side by side.

- Compile account numbers and balances.

- List recurring payments and obligations.

- Identify overlapping costs during the transition.

A well-mapped financial landscape is the first pillar of successful expat banking.

Research Banking Regulations and Requirements

Each country writes its own rules for banking, and understanding them is essential for expat banking success. Investigate the documentation required to open accounts, such as proof of address, residency status, or tax identification numbers.

Check whether your current bank allows non-residents to maintain accounts or if closure is mandatory. Learn about global compliance standards like FATCA and CRS, which can impact how and where you bank. After regulatory changes like Brexit, many banks closed accounts for EU-based clients, illustrating the importance of preparation.

For deeper insights on managing these complexities, explore Expatriate management insights to understand the broader landscape of financial compliance and expat transitions.

Plan for Account Access and Continuity

Notify your home bank about your move to prevent unexpected account freezes or flagged transactions. Set up robust online and mobile banking, including two-factor authentication and secure password recovery.

Order international debit or credit cards that feature chip and contactless technology, ensuring you can access funds globally. For instance, a US expat in Spain might test their bank’s mobile app overseas and order a travel-friendly card in advance.

- Update contact details for all banks.

- Activate digital banking features.

- Request cards suitable for international use.

A seamless expat banking experience depends on preparing your digital and physical access points before departure.

Understand Currency and Transfer Needs

Identify which currencies you will earn, spend, and save in, as expat banking often involves juggling multiple monetary systems. List regular transfer needs, such as rent, tuition, or supporting family, and calculate the typical fees and exchange rates using comparison tools.

Consider both the initial large transfers, like housing deposits, and ongoing remittances. Currency volatility surged by 20% in 2024-2025, so understanding your exposure is vital. Mapping these flows helps you minimize loss and maximize value.

- List all required currencies.

- Estimate transfer frequencies and amounts.

- Research provider fees and timelines.

A proactive approach to currency management is a hallmark of effective expat banking.

Gather Required Documentation

Successful expat banking relies on having the right paperwork ready, both digitally and in hard copy. Secure certified copies of your passport, visa, proof of address, employment contracts, and tax IDs.

Prepare for remote onboarding by scanning all documents in advance. For example, an Australian relocating to the UAE may need certified copies to open accounts before arrival.

- Digitize and back up documents.

- Organize files for quick access.

- Confirm document validity with your new bank.

Having documentation at your fingertips streamlines the banking transition and prevents delays.

Set Up Emergency and Contingency Plans

Plan for the unexpected by keeping a backup credit card and emergency cash in both home and destination currencies. Research international customer support contacts for all your banks, and note the local embassy’s details for urgent financial situations.

- Carry backup cards and emergency cash.

- Save support contact numbers.

- Know where to turn in a crisis.

These final steps create a safety net, ensuring your expat banking journey remains secure and resilient, no matter what surprises arise.

Step 2: Choose and Open the Right Expat Bank Accounts

Navigating expat banking is about more than just opening a new account. It is about designing a financial ecosystem that supports your global lifestyle. With so many banking options, features, and regulations to consider, choosing wisely can mean the difference between seamless transitions and stressful complications. Let us explore the essential steps to open the right expat bank accounts and set yourself up for financial confidence abroad.

Compare International, Offshore, and Local Bank Accounts

The expat banking landscape offers a variety of account types, each with unique advantages. International banks such as HSBC Expat and Standard Bank offer multi-currency accounts with global access, while offshore banks in locations like Jersey or the Isle of Man provide privacy and flexible residency requirements. Local banks specialize in host country needs, and digital-only banks like Wise and Revolut deliver convenience and mobile-first flexibility.

| Account Type | Pros | Cons |

|---|---|---|

| International | Multi-currency, global access | Higher fees, strict criteria |

| Offshore | Privacy, flexible residency | Regulation risk, may lack ATMs |

| Local | Local services, in-person support | Language barriers, limited intl features |

| Digital-Only | Fast setup, low fees, mobile features | Limited physical presence |

Choosing the right expat banking mix can help you manage your money confidently.

Open Accounts Before Departure When Possible

For expat banking, opening accounts before your move brings peace of mind. Remote onboarding means you can receive your first salary, set up utilities, and handle deposits as soon as you arrive. Most international and digital banks offer online applications, but you will need to prepare documents such as your passport, proof of address, and evidence of income.

Imagine a Canadian relocating to the EU who opens a Standard Bank Optimum Account online before departure. This approach reduces stress and ensures uninterrupted access to funds. Planning ahead in expat banking prevents last-minute surprises and makes your transition smoother.

Structure Your Accounts for Dual Financial Lives

Expat banking often means maintaining financial ties in two countries. Structure your accounts to separate local spending from home-country obligations. For example, keep one account for routine expenses like rent and groceries, and another for managing loans or insurance back home.

Automate regular transfers between accounts to avoid missed payments. A UK expat in Hong Kong might keep a GBP account for a UK mortgage and a HKD account for daily expenses. This approach ensures you meet your commitments on both sides, making expat banking more manageable.

Consider Digital-Only and Fintech Solutions

Digital innovation has transformed expat banking. Digital-only banks and fintech platforms like Wise, Revolut, and SuitsMe offer rapid setup and fewer barriers for proof of address. They are particularly valuable for newcomers who need instant access and mobile-first features.

The popularity of digital solutions is soaring, with digital banking users projected to reach 216.8 million in the U.S. by 2025. These platforms often provide multi-currency wallets, low transfer fees, and user-friendly apps. For expats, choosing digital solutions can unlock flexibility and cost savings in their expat banking journey.

Evaluate Account Features and Fees

Not all expat banking solutions are created equal. Compare account features carefully. Look for multi-currency wallets, debit cards with global ATM access, and accounts with no foreign transaction fees. Evaluate interest rates, minimum balance requirements, and the quality of customer support.

For instance, HSBC Expat provides GBP, EUR, and USD accounts, global debit cards, and robust online support. Choosing accounts with the right blend of features and transparent fees ensures your expat banking experience is both efficient and rewarding.

Prepare for Possible Account Closures or Restrictions

A critical step in expat banking is understanding your home bank’s policies about non-resident status. Some banks, especially after regulatory shifts, may close your account once you move. Always keep alternatives ready, such as an international or digital bank account.

After Brexit, many UK expats in the EU lost access to domestic accounts unexpectedly. By diversifying your expat banking solutions, you protect yourself from sudden disruptions and maintain control of your financial well-being.

House of Peregrine: Community Support for Expat Banking

No one should feel isolated when navigating expat banking. The House of Peregrine community offers guides, podcasts, and a network of peers to help you adapt to new banking systems and overcome cross-border challenges. Members share real experiences and trusted provider recommendations, making your financial transition smoother.

This support ecosystem empowers expats to thrive, both financially and socially, wherever life leads. With House of Peregrine, you are not alone in your expat banking journey.

Step 3: Manage Currency, Transfers, and Exchange Risks

Navigating global finances as an expat is both an art and a science. Mastering expat banking means understanding how to move money across borders with confidence, clarity, and finesse. Each step in this journey safeguards your financial well-being and transforms the ordinary into the extraordinary.

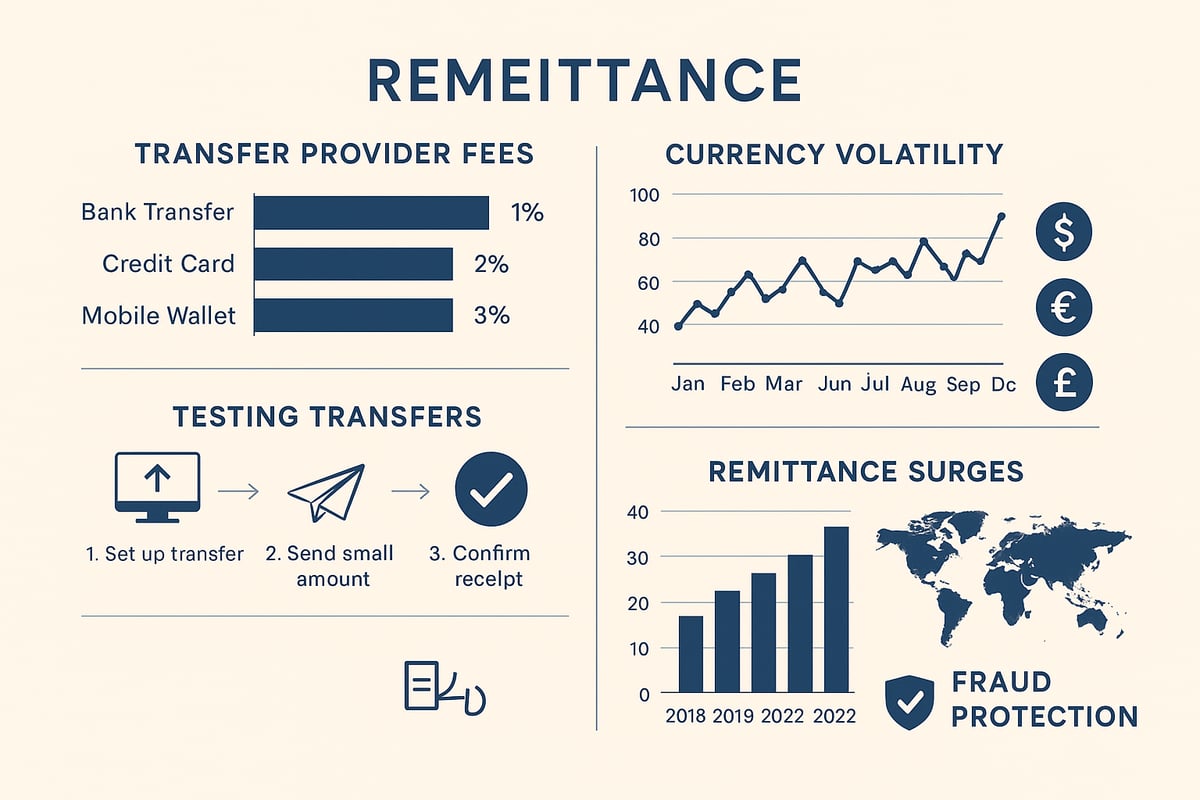

Select the Right Currency Exchange and Transfer Providers

Choosing the right partner for your cross-border transfers is essential in expat banking. Banks may offer convenience, but specialist providers often deliver superior exchange rates, lower fees, and dedicated support.

Consider the scale of global movement: Expat remittances from Saudi Arabia surged to $38.5 billion in 2024, underscoring the importance of efficient, secure solutions. Compare banks, brokers, and digital platforms for transparency and speed.

A quick table can help clarify options:

| Provider Type | Pros | Cons |

|---|---|---|

| Banks | Familiar, regulated | Higher fees, slower |

| Brokers | Better rates, support | Setup needed |

| Digital | Instant, low cost | Limits, app reliance |

Prioritize FCA-regulated providers and always read reviews before selecting your expat banking partner.

Hedge Against Currency Volatility

Currency fluctuations can quietly erode the value of your hard-earned money. In expat banking, hedging tools like forward contracts let you lock in rates for future transfers, shielding you from sudden shifts.

Set up rate alerts to catch favorable moments and consider keeping funds in multi-currency wallets, reducing the need for repeated conversions. This approach is especially powerful if you earn in one currency and spend in another.

Financial serenity comes from proactive planning, not wishful thinking. By integrating these strategies into your expat banking routine, you preserve both your wealth and your peace of mind.

Test Transfers Before Sending Large Amounts

A single misstep can turn a routine transfer into a costly headache. In expat banking, always send a small test payment before moving large sums. This confirms that beneficiary details, such as IBAN or SWIFT codes, are correct and that your provider’s process is smooth.

Keep digital and physical records of payee information in secure locations. Think of this as a dress rehearsal before the grand performance—minor errors caught early mean major issues avoided later. This habit is a hallmark of seasoned expat banking professionals.

Separate Home and Host Country Financial Flows

The duality of expat life demands financial organization. In expat banking, separating your home and host country accounts streamlines everything from rent payments to loan obligations.

Automate regular transfers for recurring expenses—rent, tuition, mortgages—using scheduled payments or standing orders. Utilize budgeting apps to track spending across multiple currencies.

This clear division creates a harmonious financial rhythm, letting you savor your global journey without distraction. Expat banking thrives on clarity and structure.

Monitor Transfer Timelines and Fees

Time is money, especially when urgent payments cross borders. In expat banking, understanding provider timelines, daily limits, and hidden charges prevents unwelcome surprises.

Public holidays, banking cut-off times, and compliance checks can delay your transfers. Choose providers that offer real-time tracking and responsive customer support.

Keep a checklist:

- Confirm daily and monthly limits

- Check for weekend or holiday delays

- Review all fee schedules

Vigilance in these details ensures your expat banking experience remains smooth and stress-free.

Protect Against Fraud and Scams in Cross-Border Transfers

Security is the cornerstone of expat banking. Only use providers regulated by authorities such as the FCA. Beware of unsolicited requests for transfers, and always verify provider credentials directly.

Phishing attempts and fake platforms target global citizens more than ever. If in doubt, contact your provider’s official support before acting.

A layered defense—secure passwords, two-factor authentication, and trusted providers—fortifies your expat banking journey, turning risk into resilience.

Step 4: Secure and Access Your Accounts from Anywhere

Managing expat banking in 2026 means weaving together security, access, and adaptability. As you step into your global chapter, safeguarding your money and ensuring seamless access are essential. Let’s explore how to protect your financial world, wherever you roam.

Set Up Robust Online and Mobile Banking

Begin your expat banking journey by fortifying your digital access. Install your bank’s apps on all devices and check compatibility with international SIM or eSIM cards. Activate biometric logins, two-factor authentication, and create unique, complex passwords.

Store recovery codes and backup methods in a secure location, such as a password manager. This preparation ensures you can always reach your accounts, even if your phone or number changes. A well-organized digital setup is the first line of defense for expat banking.

Maintain Home Country Accounts Where Possible

Keeping home country accounts active can be a lifeline for expat banking. They preserve your credit history, simplify bill payments, and offer a safety net for emergencies. Before you move, tell your bank about your relocation to prevent fraud alerts or freezes.

For example, a UK expat might keep a GBP credit card open for subscriptions or urgent needs. This dual-country approach gives you flexibility and peace of mind, especially when navigating new financial landscapes.

Prepare for Account Closures or Restrictions

Some banks limit services or close accounts when you become a non-resident. Review your bank’s policies on expat banking before you go. If closure is likely, open backup accounts with international, offshore, or digital providers.

Diversifying your banking relationships reduces the risk of losing access unexpectedly. Many expats have faced sudden account restrictions after regulatory changes, so plan ahead to keep your finances flowing smoothly.

Stay Safe from Cyber Threats

Protecting your expat banking from cyber risks is nonnegotiable. Avoid using public Wi-Fi for banking and always connect through a trusted VPN. Regularly update your apps and check accounts for unusual activity.

Consider using password managers and dedicated authenticator apps for added security. For a deeper dive into digital safety best practices, explore this Online security for expats resource. By staying vigilant, you shield your finances from evolving threats.

Manage Authentication and Communication Challenges Abroad

Relying on SMS for two-factor authentication can be unreliable overseas. Switch to authenticator apps or hardware tokens, which work even without mobile service. Keep a backup SIM or eSIM ready for critical account access.

For example, an expat in the UAE might set up Google Authenticator to access UK accounts without needing SMS codes. Proactive planning ensures you’re never locked out of your expat banking, no matter where you are.

Plan for Emergency Access and Support

Unexpected events can disrupt even the best-laid plans. Save local and international customer support numbers for all your banks. Know your local embassy’s contact information for urgent financial issues, such as lost or stolen cards.

Keep a backup card and a small reserve of emergency cash in both home and host country currencies. These simple steps provide a safety net, helping you navigate any expat banking crisis with confidence.

Step 5: Optimize, Monitor, and Stay Informed for Long-Term Success

Navigating expat banking is not a one-time task but an ongoing journey. Mastery comes from steady attention, regular tune-ups, and a willingness to adapt as your global life evolves. Let’s explore the essential habits that keep your financial world secure, nimble, and ready for whatever comes next.

Regularly Review Account Structures and Needs

Your expat banking setup should evolve with your life. Every six to twelve months, take stock of all your accounts, cards, and services. Are you still getting the best rates and features? Close dormant accounts to reduce risk and trim unnecessary fees.

- List all active accounts and note their purposes.

- Compare current fees, interest rates, and customer service quality.

- Consider whether a global or digital bank would better suit your latest location.

A digital nomad in Asia, for example, might start with a local bank but switch to a global fintech after discovering better international options. This regular review ensures your expat banking remains an asset, not a liability.

Track Exchange Rates and Economic Trends

Global economic tides can shift quickly, directly impacting your expat banking experience. Monitor exchange rates, inflation, and political changes that influence currencies. Use tools and alerts to time large transfers wisely.

According to the Bank for International Settlements, global cross-border bank credit reached $45 trillion in Q3 2025, highlighting the immense flow of money across borders and the need for vigilance. A sudden swing could turn a routine transfer into a costly lesson, so staying informed keeps your finances resilient.

Stay Up-to-Date with Banking Regulations

The rules of expat banking are always changing. Subscribe to newsletters, join forums, and check for updates from your banks. Regulations like FATCA, CRS, and local tax laws shift frequently, affecting account access and compliance.

By early 2025, over 78 countries have implemented open banking frameworks, transforming how data and money move worldwide. Staying ahead of these changes protects your access and ensures you meet all requirements.

Leverage Community and Expert Resources

No one should navigate expat banking alone. Tap into expat communities, online groups, and professional networks. These spaces offer real-time advice, peer support, and firsthand insight into local banking quirks.

- Join webinars or workshops focused on financial strategies.

- Ask questions in online forums about new regulations or providers.

- Share your own experiences to help fellow expats.

The collective wisdom of the global expat community is a powerful resource for mastering expat banking.

Avoid Common Pitfalls and Scams

Scams targeting expats are on the rise, especially as banking becomes more digital and borderless. Always verify credentials before opening new accounts or sending funds. Watch for high-fee offers or promises that sound too good to be true.

- Use only regulated, well-reviewed providers.

- Be cautious with unsolicited emails or messages about transfers.

- Read reviews and seek referrals from trusted expat sources.

Staying vigilant is an essential part of safe expat banking.

Plan for Future Moves and Global Mobility

Think of expat banking as your portable toolkit. Choose accounts that can move with you, minimizing disruption during future relocations. Keep digital and physical records organized for easy transitions.

A family moving between Singapore, the UK, and the US, for example, benefits from international banks that streamline account management across borders. Planning ahead ensures you’re never caught off guard by a sudden move.

Seek Professional Advice When Needed

Complex financial lives call for expert guidance. When your expat banking needs become intricate, consult with international financial advisors or expat-focused CPAs. They can clarify tax obligations, compliance, and investment strategies.

Many firms offer free discovery calls or initial consultations. Taking advantage of professional advice can transform uncertainty into confidence, supporting your financial wellbeing wherever you land.

Frequently Asked Questions About Expat Banking

Navigating expat banking can feel like charting a course through unfamiliar waters. With so many choices and evolving regulations, finding clarity is key. Below, we answer the most pressing questions global citizens ask about expat banking, so you can move forward with confidence and ease.

What is the best bank account for expats?

There is no universal “best” solution in expat banking. The right account depends on your destination, income sources, and lifestyle. International and offshore accounts, such as Standard Bank Optimum or HSBC Expat, offer multi-currency support and global access. Digital banks like Wise or SuitsMe are ideal for those who may lack local proof of address.

Quick comparison:

| Account Type | Multi-Currency | Remote Setup | Fees |

|---|---|---|---|

| International Bank | Yes | Yes | Moderate |

| Offshore Account | Yes | Yes | Varies |

| Digital Bank | Yes | Yes | Low |

| Local Bank | Rarely | Sometimes | Varies |

Can I keep my home country bank account while living abroad?

Often, yes, you can maintain your home country account while abroad. However, expat banking rules vary. Some banks need notification of your new address, while others may restrict or close accounts for non-residents. For example, many UK expats in the EU lost accounts after Brexit. Keeping your account open helps with credit continuity and emergency access.

Will my bank close my account when I move abroad?

It is possible, especially after regulatory changes. Many expats have faced sudden closures, so always check your bank’s non-resident policies before relocating. Maintain backup options, such as international or digital accounts, in case your primary account is closed. Being proactive is essential for uninterrupted expat banking.

What is a multi-currency account, and do expats need one?

A multi-currency account lets you hold, spend, and receive funds in several currencies without constant conversion. For many, multi-currency support is the cornerstone of seamless expat banking. This flexibility helps you avoid frequent exchange fees and suits those with cross-border obligations. Providers like Wise and Revolut make it easy to manage multiple currencies from one platform.

Which banks have no foreign transaction fees for expats?

Traditional banks often charge hidden fees for global transactions. However, some digital banks and currency specialists offer fee-free or reimbursed ATM withdrawals. When choosing expat banking providers, compare fee structures carefully. Many expats prefer digital options for transparent pricing and global-friendly features.

How can I transfer money abroad safely and cheaply?

For safe and affordable cross-border transfers, consider regulated currency specialists. They often provide better rates and lower fees than traditional banks. Use FCA-licensed or similarly regulated services, set up forward contracts or alerts for favorable rates, and always verify provider credentials. For complex or high-value transfers, consulting a CPAs for expats guide can ensure compliance and peace of mind.

Can I open a bank account abroad without proof of address?

Some digital and international banks allow you to open an account without a local address, which is especially useful for new arrivals. Providers like Wise and SuitsMe offer streamlined onboarding for expat banking clients, letting you access funds and pay bills quickly, even before securing permanent accommodation.

Additional Resources and Support

Choosing the right support network is vital for successful expat banking. Explore reputable provider comparison tools, join expat communities, and seek guidance from professionals. If you need tailored help with relocation or financial transitions, consider reading an expat relocation services overview for expert insights on banking, compliance, and settling abroad.

As you navigate the intricate path of expat banking and global living, remember that you’re not alone on this journey. Embracing change and mastering your finances abroad is so much more rewarding when you’re connected with others who truly understand the adventure. Imagine a place where guidance, inspiration, and connection flow as seamlessly as your cross-border transfers a community that celebrates every step of your international life. If you’re ready to deepen your roots and expand your world, House of Peregrine is the network for International life, created by and for people living abroad. Get started with a FREE account today to unlock exclusive content, connections, and opportunities: Join a global circle of thinkers, creators, and doers. We host events, build products, publish guides, run a podcast, offer rewards and curated products — all within a vibrant ecosystem of experts and businesses to support your life abroad.